DSCR Loans Florida

Nov 6, 2023, 12:48 IST

DSCR Loans Florida

DSCR Loans Florida or anywhere else refers to the Debt Service Coverage Ratio (DSCR). These loans are financial products designed to assess and secure financing for real estate investments, particularly in the commercial real estate sector. The Debt Service Coverage Ratio (DSCR) is a critical metric in these loans. The DSCR is a measure of a property's ability to generate enough income to cover its debt obligations, including loan repayment. In the context of real estate, DSCR loans are commonly used to finance income-producing properties, such as apartment buildings, office complexes, or retail centres. Lenders in Florida and other locations use the DSCR to evaluate the property's cash flow and determine if it can support the loan.Key points to note about DSCR loans in Florida:

1. DSCR Calculation: To qualify for a DSCR loan, borrowers need to have a DSCR that meets the lender's requirements. The DSCR is calculated by dividing the property's net operating income (NOI) by its total debt service, which includes the principal and interest payments on the loan. A DSCR greater than 1.0 indicates that the property generates enough income to cover its debt service. 2. Property Type: DSCR loans are primarily used for commercial real estate properties, such as multifamily apartment buildings, hotels, retail centres, or office buildings. These properties generate rental income that contributes to the DSCR. 3. Risk Assessment: Lenders in Florida assess the DSCR to evaluate the risk associated with the loan. A higher DSCR is typically seen as a lower risk because it shows that the property has a comfortable buffer to cover debt payments. Lower DSCR values may result in a higher perceived risk and could affect loan terms. 4. Loan Terms: The terms of DSCR loans can vary, but they often have competitive interest rates and longer repayment periods. Loan approval and terms depend on factors such as the DSCR, the borrower's creditworthiness, the property's condition, and the local real estate market. 5. Use in Property Investment: Investors in Florida use DSCR loans to acquire, refinance, or improve income-generating real estate properties. These loans provide access to capital for property purchases and renovations, allowing investors to enhance the property's cash flow and value. 6. Market Factors: The availability and terms of DSCR loans may be influenced by the local real estate market conditions in Florida. Lenders take into account the specific market dynamics when evaluating loan applications.Rishte Paisa Shayari

DSCR Calculation in Florida:

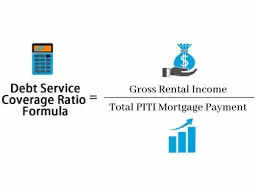

The Debt Service Coverage Ratio (DSCR) is a fundamental aspect of DSCR loans in Florida. It serves as the primary measure by which lenders assess the property's financial health and determine whether it can support the loan. DSCR is calculated by dividing the property's net operating income (NOI) by its total debt service, which includes both principal and interest payments on the loan. In Florida, as in other locations, this ratio is critical because it indicates the property's ability to generate sufficient income to meet its financial obligations. The DSCR calculation can be represented as:NetOperatingIncome DSCR= ------------------------ TotalDebtService

A DSCR value of 1.0 indicates that the property's income precisely covers its debt service. In Florida, lenders often require a DSCR of at least 1.25 to 1.35 to approve a loan. This higher DSCR requirement provides a financial buffer, ensuring that the property generates ample income to comfortably meet its debt obligations. It also offers some protection against potential fluctuations in income. Property Type in Florida: DSCR loans in Florida are commonly used to finance various types of commercial real estate properties. These properties generate income through rent or other revenue streams, making them suitable candidates for DSCR financing. Property types that frequently qualify for DSCR loans in Florida include: 1. Multifamily Apartments: Apartment buildings with multiple rental units can be financed with DSCR loans. Investors often seek these loans to acquire or improve such properties in Florida's dynamic real estate market. 2. Office Buildings: Commercial office spaces represent another significant sector for DSCR loans in Florida. Office buildings can range from small office complexes to large corporate centres. 3. Retail Centers: Shopping malls, strip malls, and individual retail spaces are prime candidates for DSCR loans. These loans can support the acquisition, development, or renovation of retail properties in Florida. 4. Hotels and Hospitality: Hotels and other hospitality properties are eligible for DSCR loans. These loans help owners invest in upgrades or acquire additional properties in Florida's tourism-focused economy. 5. Industrial Properties: Industrial facilities and warehouses that generate rental income are also considered for DSCR financing in Florida.

A DSCR value of 1.0 indicates that the property's income precisely covers its debt service. In Florida, lenders often require a DSCR of at least 1.25 to 1.35 to approve a loan. This higher DSCR requirement provides a financial buffer, ensuring that the property generates ample income to comfortably meet its debt obligations. It also offers some protection against potential fluctuations in income. Property Type in Florida: DSCR loans in Florida are commonly used to finance various types of commercial real estate properties. These properties generate income through rent or other revenue streams, making them suitable candidates for DSCR financing. Property types that frequently qualify for DSCR loans in Florida include: 1. Multifamily Apartments: Apartment buildings with multiple rental units can be financed with DSCR loans. Investors often seek these loans to acquire or improve such properties in Florida's dynamic real estate market. 2. Office Buildings: Commercial office spaces represent another significant sector for DSCR loans in Florida. Office buildings can range from small office complexes to large corporate centres. 3. Retail Centers: Shopping malls, strip malls, and individual retail spaces are prime candidates for DSCR loans. These loans can support the acquisition, development, or renovation of retail properties in Florida. 4. Hotels and Hospitality: Hotels and other hospitality properties are eligible for DSCR loans. These loans help owners invest in upgrades or acquire additional properties in Florida's tourism-focused economy. 5. Industrial Properties: Industrial facilities and warehouses that generate rental income are also considered for DSCR financing in Florida. Rishte Paisa Shayari

Risk Assessment in Florida:

The DSCR serves as a crucial tool for assessing risk in DSCR loans, and lenders in Florida use this metric to evaluate the potential risk associated with a loan application. A higher DSCR is generally seen as an indicator of lower risk because it demonstrates that the property generates more income than is necessary to cover its debt service. On the other hand, a lower DSCR may be interpreted as a higher risk, as it indicates that the property's income might be insufficient to meet its financial obligations. In Florida, as in any market, the perceived risk associated with a loan influences various aspects, such as the interest rate, loan terms, and the loan-to-value (LTV) ratio. A higher DSCR can often lead to more favourable loan terms, including lower interest rates and a higher LTV ratio. This, in turn, makes it more attractive for borrowers in Florida to secure financing for their real estate investments.Loan Terms in Florida:

Loan terms for DSCR loans in Florida can vary, depending on several factors, including the borrower's qualifications, the property's condition, and the lender's policies. However, DSCR loans in Florida often offer competitive interest rates and extended repayment periods. The specifics of these loan terms may include: 1. Interest Rates: Interest rates for DSCR loans in Florida are influenced by factors like the DSCR, the borrower's creditworthiness, market conditions, and the lender's pricing strategy. Generally, a stronger DSCR can lead to lower interest rates. 2. Repayment Period: The repayment period for DSCR loans can be longer than traditional loans. It's not uncommon for DSCR loans in Florida to have terms ranging from 15 to 30 years. This extended repayment period can be advantageous for borrowers by reducing monthly payments. 3. Loan Amount: The loan amount a borrower can secure depends on the property's DSCR, appraised value, and the lender's loan-to-value (LTV) ratio. Higher DSCR values often allow for a larger loan amount. 4. Amortization Schedule: DSCR loans may use different amortization schedules, such as a straight line or a schedule based on the property's cash flow. The choice of amortization can affect the loan's structure and payments.

1. Interest Rates: Interest rates for DSCR loans in Florida are influenced by factors like the DSCR, the borrower's creditworthiness, market conditions, and the lender's pricing strategy. Generally, a stronger DSCR can lead to lower interest rates. 2. Repayment Period: The repayment period for DSCR loans can be longer than traditional loans. It's not uncommon for DSCR loans in Florida to have terms ranging from 15 to 30 years. This extended repayment period can be advantageous for borrowers by reducing monthly payments. 3. Loan Amount: The loan amount a borrower can secure depends on the property's DSCR, appraised value, and the lender's loan-to-value (LTV) ratio. Higher DSCR values often allow for a larger loan amount. 4. Amortization Schedule: DSCR loans may use different amortization schedules, such as a straight line or a schedule based on the property's cash flow. The choice of amortization can affect the loan's structure and payments. Use in Property Investment in Florida:

DSCR loans play a vital role in property investment in Florida. Investors and property owners use these loans for various purposes: 1. Property Acquisition: Investors use DSCR loans to finance the acquisition of income-generating properties. This includes purchasing multifamily buildings, retail spaces, or office complexes in Florida's real estate market. 2. Property Improvement: DSCR loans can also be used to fund property improvements and renovations. Florida's competitive real estate market often requires property owners to upgrade their assets to remain competitive. 3. Cash Flow Enhancement: Investors may use DSCR loans to improve the cash flow of their properties. These loans can finance initiatives that attract higher-paying tenants or increase rental income. 4. Portfolio Expansion: DSCR loans allow investors to expand their property portfolios by providing the necessary capital for additional acquisitions. This is especially important in Florida's growing real estate sector. 5. Refinancing: Property owners can use DSCR loans for refinancing existing loans on favourable terms, potentially reducing monthly payments and increasing cash flow.Market Factors in Florida:

Florida's unique real estate market dynamics can impact the availability and terms of DSCR loans. The state's real estate market is known for its diversity, with tourism, hospitality, and diverse industries playing significant roles. Lenders in Florida consider these factors when evaluating loan applications: 1. Market Conditions: The current state of Florida's real estate market, including demand, property values, and rental income potential, can influence the terms and availability of DSCR loans. 2. Local Economies: Specific regions in Florida may experience different economic conditions. Lenders may tailor their loan terms to account for variations in the local economy. 3. Property Types: The types of properties in Florida, such as beachfront condos, urban office spaces, and suburban retail centres, can impact the loan options available and the associated risks. 4. Tourism and Seasonality: Florida's tourism industry, which experiences seasonal fluctuations, can affect the stability of rental income. Lenders may assess properties with these dynamics differently. 5. Market Competitiveness: In Florida's competitive real estate market, DSCR loans can provide a competitive advantage to investors looking to secure financing for high-demand properties.