How to Calculate Mortgage Rates

Mortgage rates are the interest rates charged on a mortgage loan, which are crucial because they determine the cost of borrowing. A lower mortgage rate means lower monthly payments and overall savings over the life of the loan. Understanding how to calculate mortgage rates can empower you to make informed decisions when purchasing a home.

Types of Mortgage Rates

1. FixedRate Mortgages:

The interest rate remains constant throughout the loan term, providing stability and predictability in monthly payments.

Common terms are 15, 20, and 30 years.

2. AdjustableRate Mortgages (ARMs):

The interest rate is initially fixed for a certain period (e.g., 5, 7, or 10 years) and then adjusts periodically based on market conditions.

After the initial period, rates may increase or decrease, affecting monthly payments.

3. Hybrid ARMs:

These combine features of fixed and adjustablerate mortgages, often starting with a fixed rate for a number of years, followed by adjustable rates.

Factors Influencing Mortgage Rates

1. Credit Score:

Lenders use your credit score to gauge your risk level. Higher scores usually lead to lower rates.

Scores are typically categorized as excellent (740+), good (700739), fair (620699), and poor (below 620).

2. Loan Amount and Type:

The total loan amount can affect your rate. For example, conforming loans (those that meet Fannie Mae and Freddie Mac guidelines) often have better rates than jumbo loans.

3. Down Payment:

A larger down payment reduces the lender's risk and can secure a lower interest rate. Generally, a down payment of 20% or more may help you avoid private mortgage insurance (PMI).

4. Loan Term:

Shorter loan terms usually come with lower interest rates. For instance, a 15year fixed mortgage often has a lower rate than a 30year fixed mortgage.

5. Market Conditions:

Economic indicators, inflation rates, and the Federal Reserve's monetary policy all influence mortgage rates. When the economy is strong, rates may rise; when it’s weak, rates may fall.

6. Location:

Regional factors and local real estate market conditions can also impact mortgage rates.

How to Calculate Mortgage Rates

Calculating your monthly mortgage payment requires understanding a few key terms and using a specific formula. Here’s a stepbystep guide:

1. Gather Necessary Information

Before you start calculating, collect the following:

Loan Amount (Principal): The total amount you plan to borrow.

Annual Interest Rate: The rate offered by your lender.

Loan Term: The duration of the loan in years.

2. Convert Annual Interest Rate to Monthly

To calculate the monthly interest rate, divide the annual rate by 12 (the number of months in a year):

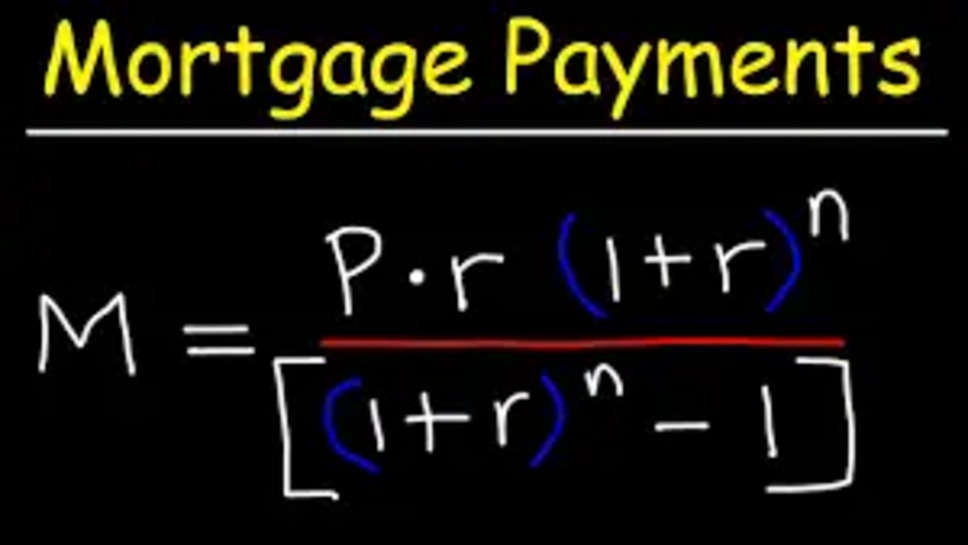

Where:

- M = Monthly payment

- P = Loan amount (principal)

- r = Monthly interest rate (as a decimal)

- n = Number of payments

Additional Costs to Consider

When budgeting for a mortgage, it’s essential to consider other costs beyond the principal and interest:

1. Property Taxes:

These are typically included in your monthly payment and can vary widely depending on your location.

2. Homeowners Insurance:

Protects your property against damages and is usually required by lenders.

3. Private Mortgage Insurance (PMI):

If your down payment is less than 20%, you may need to pay PMI, which protects the lender in case you default.

4. Homeowner Association (HOA) Fees:

If applicable, these fees can also be part of your monthly expenses.

Shop Around for Rates

To find the best mortgage rate, it’s wise to shop around with different lenders. Rates can vary significantly based on lender policies, so obtaining quotes from several banks, credit unions, and online lenders can save you money.

Understanding Mortgage Points

Mortgage points are fees you can pay upfront to lower your interest rate. One point equals 1% of the loan amount. For example, on a $250,000 loan, one point would cost $2,500.

Paying Points: If you plan to stay in your home longterm, paying points to reduce your interest rate can save you money over time.

Not Paying Points: If you anticipate moving or refinancing within a few years, it may be better to avoid points and keep your upfront costs lower.

Final Thoughts

Understanding how to calculate mortgage rates and the factors influencing them is vital for any homebuyer. By gathering necessary information, using the correct formulas, and considering all associated costs, you can make informed decisions about your mortgage.

While calculating your potential monthly payments is essential, always consult with a financial advisor or mortgage professional for personalized advice tailored to your financial situation. This ensures that you choose the best mortgage product for your needs and ultimately secure the most favorable terms.